Harnessing multi-speed growth and divergent dynamics

As we look towards the rest of the year, restrictive monetary policies and reduced fiscal expansion are curbing inflation without triggering a recession. Central banks are now set to cut rates to prevent excessive economic slowdown, despite uncertainties from varying growth rates, persistent inflations, limited fiscal space, and geopolitical risks.

The global economic outlook is mixed, with the US slowing, the EU recovering, China in a controlled slowdown, and strong growth in countries like India.

Monica Defend

In a world with decelerating but sticky inflation and multi-speed growth, Central Banks will need to carefully assess their stance and communication. Their actions may not be synchronised, but we expect any divergences to be limited.

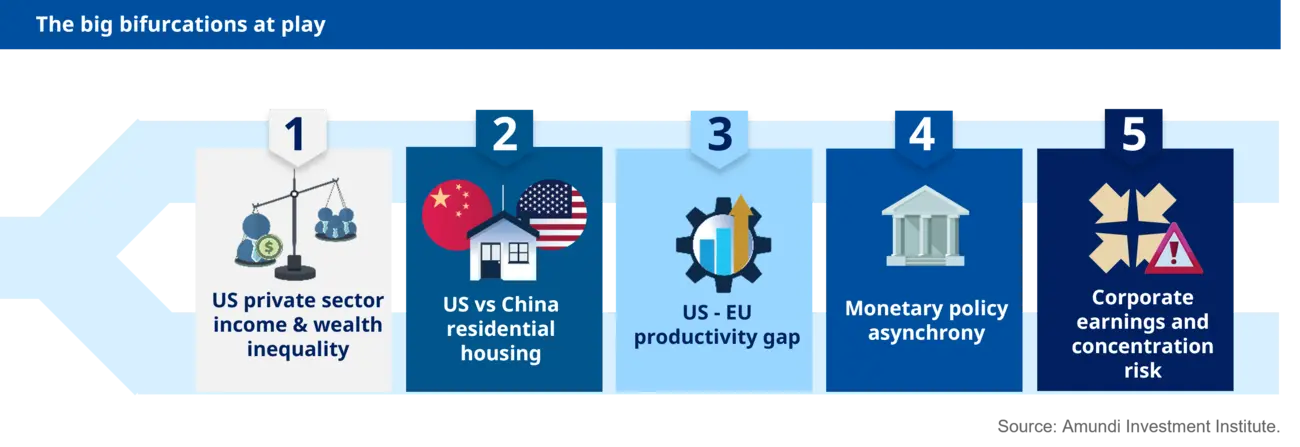

7 themes to keep an eye on

Global growth is expected to reach 3.1% in 2024. However, there are divergences in play: the US is slowing down (without a recession), the Eurozone is on a recovery path, India's strong growth continues while China is on a controlled slowdown trajectory. Inflation has been stickier than expected, but it is expected to further decelerate and reach central bank targets in 2025. This will allow central banks to initiate and continue the new cycle of cuts at different speeds.

Geopolitical risk is expected to increase in the coming years, with factors such as protectionism, sanctions, tariffs, export controls and trade wars intensifying and not all regions (notably Europe) being in a position to afford them. The outcome of the US election will be pivotal, as US foreign policy in particular (including trade) is expected to differ significantly under a Biden or a Trump presidency, although confrontation with China is expected to rise in any case.

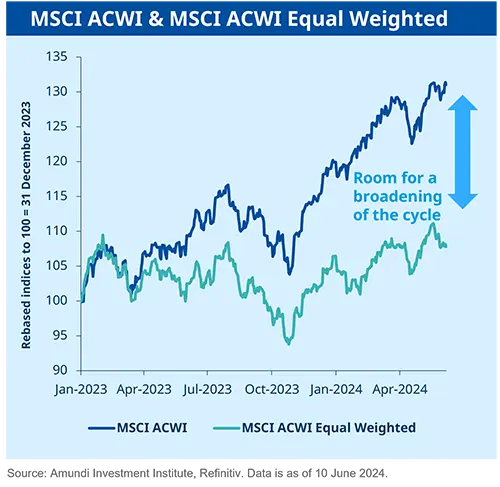

Equities are still attractive, unless we enter a recession. However, there are concerns about excessive valuations in US mega caps. Opportunities abound in US quality value and international equity. In Europe, consider small-cap stocks to capitalize on the economic cycle recovery and attractive valuations.

After trading in a narrow range, yields are set for a new course with rate cuts approaching and curves expected to structurally steepen. With yields already at historically appealing levels this offer a window of opportunities. We favour government bonds and investment grade credit which keeps the best risk/reward profile. EM bonds also offer an attractive risk-return profile and will benefit from the Fed cuts in the second semester.

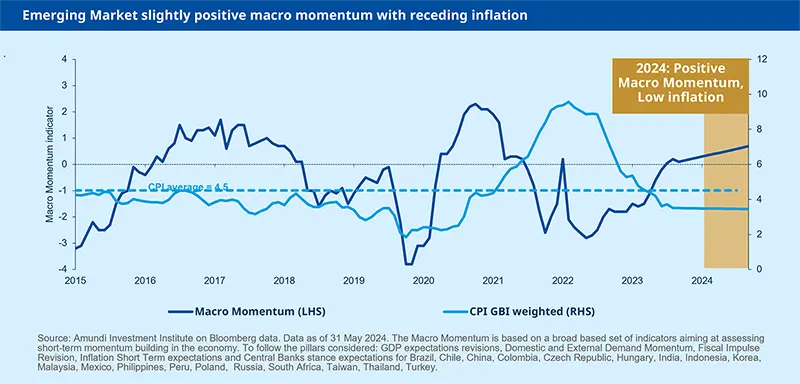

With resilient growth, supply chain rebalancing, and Fed rate cuts, Emerging Market equities offer interesting opportunities supported also by attractive valuations compared to the US. We favour Latam and Asia, with India in focus thanks to its robust growth and transformative trajectory. Bonds also will be lifted by Fed cuts, with local currencies set to become attractive.

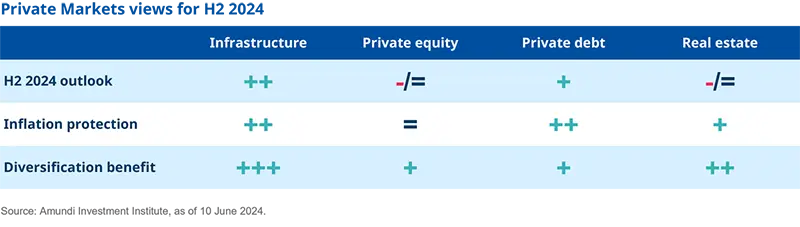

It's time to strike a balance between opportunities from supportive earnings dynamics and appealing bond yields with risks from high uncertainty on both growth and inflation fronts. This means combining a positive equity stance with a long duration bias and searching for additional sources of diversification, such as commodities and real and alternative assets, including hedge funds. These assets will be key to enhancing the risk-return portfolio profile.

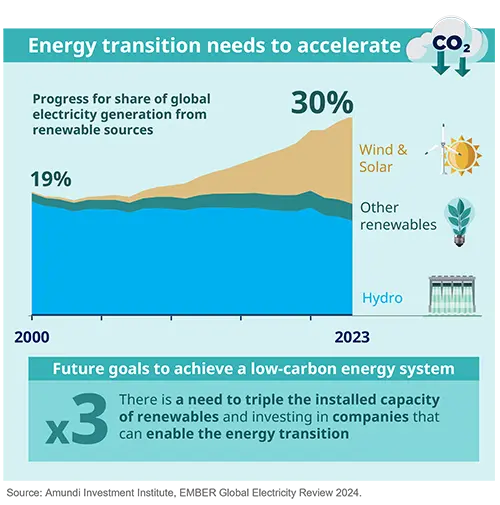

To achieve a low-carbon energy system, the world must triple renewable capacity by 2030.

This means investing heavily in critical minerals and expanding electricity grids. Investors should focus on companies that can enable the energy transition in both developed and emerging markets.

Investment Convictions from our CIOs

Despite the uncertain outlook, some regional markets are priced for the best outcome. We favour asset allocations that can withstand various scenarios. Equities, except for US mega caps, remain attractive, with emerging markets supported by valuations and potential Fed easing. Fixed income also presents an opportunity due to historically appealing yields. Additional diversification can be found in commodities, as well as real and alternative assets.

Dynamic asset allocation in a late cycle with inflation risk

Bonds' appeal with central banks at a turning point

Broaden the opportunity set in equities

EM winners in a fragmented world

Energy transition and structural themes

Diversify with real and alternative assets

Vincent Mortier

The economic context supports earnings and risky assets, but much of the upside potential is already priced in and finding clear catalysts for further gains is challenging.

Explore our 2024 Mid-Year Outlook

Geopolitics: A new window of vulnerability opens in the second half of the year

Emerging markets: EM winners in a fragmented world

management and works closely with in-house

fund management teams & advisory services

on a variety of topics.

Jogi Nyilatkozat Marketingközlemény/Forgalmazási közlemény. Jelen megjelenés elemei kizárólag tájékoztatás céljára készültek, azok nem minősülnek pénzügyi eszközök vételére/eladására tett ajánlatnak, befektetési tanácsnak, befektetési elemzésnek, befektetési ajánlásnak, vagy egyéb befektetési szolgáltatás nyújtására vonatkozó ajánlatnak, illetve adójogi tanácsadásnak és nem adnak teljes körű tájékoztatást az itt szereplő kibocsátókkal, pénzügyi eszközökkel, ügyletekkel kapcsolatban. Ha nincsen másképp feltüntetve, jelen aloldalon szereplő valamennyi információ az Amundi Asset Management S.A.S-től származik. A piaci meglátások a szerzőtől származnak, nem feltétlenül tükrözik az Amundi Csoport véleményét. A tájékoztatás olyan forrásokon alapult, melyet a szerző a felhasználás időpontjában megbízhatónak ítélt, de azok a gazdasági és egyéb körülményektől függően bármikor változhatnak. Nincs rá biztosíték, hogy az egyes országok, piacok vagy ágazatok a várakozásoknak megfelelően fognak alakulni, mint ahogy arra sem, hogy a tájékoztatásban bemutatott piaci előrejelzések megvalósulnak, illetve a most tapasztalt piaci folyamatok változatlanok maradnak. Az Amundi Csoport SFDR-rel (az Európai Parlament és a Tanács a pénzügyi szolgáltatási ágazatban a fenntarthatósággal kapcsolatos közzétételekről szóló 2019. november 27-i (EU) 2019/2088 Rendelete) kapcsolatos) álláspontjáról a mindenkor hatályos Felelős Befektetési Politikája és az SFDR jogszabályi rendelkezések alapján kialakított közzétételi nyilatkozata nyújt tájékoztatást. A dokumentumok elérhetősége: www.amundi.com. Az Amundi Csoport által kezelt nemzetközi alapok esetében az adott termék Tájékoztatójában, annak „Fenntartható befektetés” című fejezetében találhatók, melyek elérhetősége: www.amundi.com/ www.amundi.lu Bár az Amundi különös gondot fordított a jelen aloldalon foglaltak kialakítására, annak pontosságáért, helyességéért, teljességéért, vagy tényállításként történő felfogásáért semmilyen jogcímen - kifejezett vagy vélelmezhető - felelősséget nem vállal. Az Amundi felhívja figyelmét, hogy az itt megjelenő tájékoztatást csak saját kockázatára használhatja fel, az arra támaszkodó döntéshozatalból az olvasó által elszenvedett esetleges veszteségért, elmaradt haszonért az Amundi Csoporthoz tartozó vállalatokat, vagy azok bármely tisztségviselőjét semmilyen – közvetlen vagy közvetett – jogi felelősség nem terheli. A befektetések kockázattal – többek között politikai és devizakockázattal – járnak. Kérjük, vegye figyelembe, hogy befektetésének értéke emelkedhet, illetve csökkenhet is, és akár a teljes befektetett tőke elveszhet. A múltbeli teljesítmény alapján nem jelezhetőek előre a jövőbeli hozamok. A diverzifikáció nem garantálja a nyereséget, illetve nem véd a veszteségtől. Nincs garancia arra, hogy az ESG megfontolások javítják egy adott befektetés teljesítményét. A befektetőnek a befektetésről szóló döntésük során figyelembe kell venniük az adott befektetés összes jellemzőjét vagy célkitűzését, így különösen a befektetés tárgyát, kockázatát, díjait és a befektetésből származó esetleges károkat. Az elért jövőbeli teljesítményt adó terhelheti, amely az egyes befektetők személyes helyzetétől függ és a jövőben változhat. Befektetési döntéséhez és a befektetés jövőbeli hozamához kapcsolódó adószempontok elbírálásához javasoljuk, hogy kérje ki szakértő, vagy adótanácsadó véleményét. Az aloldalon szereplő tájékoztatást az Amundi előzetes írásbeli jóváhagyása nélkül tilos másolni, reprodukálni, módosítani, lefordítani vagy terjeszteni, a tartalmat az Amundi előzetes értesítés nélkül jogosult aktualizálni vagy megváltoztatni. Jelen felület nyomtatási és elütési hibát tartalmazhat.